THE CASE FOR TRADE WARS

Why The U.S. Has The Upper Hand

Economic Impacts of a US–China–EU Tariff Escalation (2025–2030)

1. Limited Macroeconomic Gain from Low Foreign Tariffs

The U.S. economy’s reliance on exports is relatively low – exports of goods and services constitute only about 10–12% of U.S. GDP. By comparison, many advanced economies depend on exports for 20–50% of GDP (e.g. China ~20%, Germany ~47%). This means that foreign tariff reductions (which make U.S. exports more competitive abroad) provide only modest direct benefits to overall U.S. growth. Even if U.S. exports increase due to lower foreign tariffs, the boost to GDP is small given exports’ small share. As one analysis noted, “US growth does not rely much on exports (exports are only 12% of GDP)” – domestic consumption and investment are far bigger growth drivers. Moreover, U.S. multinational companies often serve foreign markets by local production or supply chains rather than solely via exports from the U.S., further muting the impact of foreign tariffs on the broader U.S. economy.

By contrast, export-driven economies are more sensitive to foreign tariffs. For example, Germany’s growth model is heavily trade-dependent, with exports nearly half of its GDP. China’s exports are about one-fifth of its GDP (and were an even larger share in past decades). These countries see significant gains when trading partners lower tariffs – and significant pain when tariffs rise – because trade is a large component of their economic activity. The U.S., with its vast domestic market, has a built-in buffer against trade disruptions: roughly 88–90% of U.S. GDP comes from domestic consumption and investment. In other words, low foreign tariffs and expanded export access, while helpful to certain U.S. industries, do not dramatically move the needle for the overall U.S. economy. This asymmetry sets the stage for the U.S. having more leverage in a tariff standoff, as discussed later.

2. Short-Term Pain: Higher Input Costs for U.S. Manufacturers and Consumers

In the initial phases of a tariff escalation, American manufacturers and consumers would face higher costs. Tariffs are essentially a tax on imported goods – whether they are consumer products on store shelves or intermediate inputs used by U.S. factories. When the U.S. raises tariffs on foreign parts, materials, or finished goods, import prices rise. Evidence from recent trade disputes shows U.S. companies and households end up paying much of these costs. For example, during the 2018–2019 U.S.–China trade war, U.S. domestic production slowed and consumer prices rose as tariffs took effect. The Federal Reserve’s industrial production index for manufacturing declined year-on-year in 2019 – the first contraction since 2015 – partly due to tariff-induced supply chain disruptions and higher input costs. U.S. firms had to pay more for tariffed components and materials, squeezing profit margins or forcing them to raise prices.

Consumers likewise felt the pinch. Academic and government studies of the 2018–2019 tariffs found that the tariffs’ costs were largely passed through to U.S. buyers in the form of higher prices, contradicting assertions that foreign exporters would absorb the costs. In effect, tariffs function as a regressive tax on consumption, hitting price-sensitive goods from electronics to apparel. One analysis estimated a net welfare loss to the U.S. economy equivalent to about $1.4 billion per month in forgone consumption during the height of the China–U.S. tariff battle. In summary, the short-run impact of higher U.S. tariffs is a supply shock: American producers face costlier inputs (like machine parts, semiconductors, aluminum, etc.), and consumers pay more for imported finished goods (from clothing to electronics). This creates a drag on growth and household welfare in the immediate term, before economies have time to adjust.

3. Supply Chain Substitution: Shifting Sources of Key Imports

Over a 2025–2030 horizon, the U.S. would seek to mitigate tariff damage by replacing Chinese and European imports with supplies from other countries. The feasibility of this substitution varies by sector, but lessons from recent years inform what could happen:

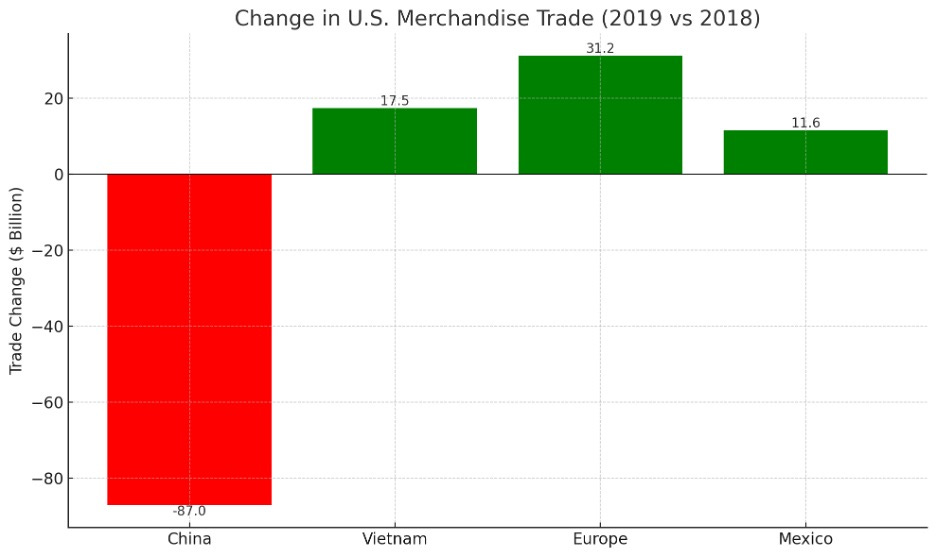

Electronics and Electrical Equipment: China is a dominant supplier of electronics, but alternatives have been scaling up. Vietnam, Taiwan, Malaysia, Mexico, and others have expanded production in response to previous U.S. tariffs on China. In 2019, U.S. imports from China dropped sharply (a reduction of $87 billion, or –16% year-on-year) as tariffs hit, but other countries partially filled the gap. Vietnam’s exports to the U.S. jumped by 35% that year (an increase of ~$17.5 billion), and Taiwan also saw significant gains, especially in electronics components. By 2019, of about $31 billion in manufacturing imports that the U.S. shifted away from China to other Asian “low-cost countries,” Vietnam alone absorbed 46% of that shift (roughly $14 billion). This trend suggests that if the U.S. raises tariffs on Chinese high-tech goods, it can turn to suppliers like Vietnam, Taiwan, South Korea, and Mexico for electronics assembly and parts. Indeed, U.S. imports of electronics from Vietnam nearly doubled from 2018 to 2019, and by 2024 the U.S. was importing $127 billion in electrical machinery from China’s competitors, reflecting supply chain diversification.

Machinery and Equipment: Heavy machinery and capital equipment from Europe (e.g. German factory tools) could be replaced over time with imports from Japan, South Korea, or domestic production. Mexico is a key alternative for automotive parts and machinery due to integrated North American supply chains. India and Southeast Asia are also ramping up production of industrial machinery and chemicals, offering potential long-term substitutes if European imports become pricier.

Autos and Auto Parts: If tariffs hit European autos, American buyers could shift toward cars made in Japan, South Korea, Mexico, or domestic U.S. models. Notably, German automakers already produce many vehicles in the U.S. (BMW’s Spartanburg plant is its largest globally), so higher tariffs on imported European-made cars might accelerate localization. The U.S. could also import more from non-European luxury brands (Lexus, Acura, Genesis, etc.) to satisfy high-end demand. In auto parts, Mexico and Canada (under USMCA) are natural alternate sources, as are suppliers in East Asia.

Medical Devices and Pharmaceuticals: The U.S. imports medical equipment from Europe (e.g. imaging machines, precision instruments) and basic pharmaceuticals from China/India. Tariffs in these areas could spur greater sourcing from countries like Ireland, Switzerland (for high-end pharma/medtech), or increased domestic stockpiling and production of critical medical supplies. Countries such as India (already a major generic drug supplier) could capture more U.S. market share if Chinese pharma inputs face tariffs.

Textiles and Consumer Goods: Many low-end consumer goods (apparel, footwear, home goods) have already diversified away from China to countries like Vietnam, Bangladesh, India, and Indonesia. Tariffs would accelerate this shift. For instance, even before 2025, China’s share of U.S. apparel imports had fallen significantly, replaced by Vietnam and Bangladesh. Retail supply chains are quite adaptable in this segment, chasing lower-cost producers—so a tariff-induced squeeze on Chinese textiles would likely benefit South/Southeast Asian exporters. Central America (for textiles) and Mexico (for appliances, furniture) could also scale up to serve U.S. demand.

It’s important to note that supply chain substitution is not instantaneous or costless. There are capacity constraints – e.g. Vietnam’s manufacturing GDP is an order of magnitude smaller than China’s, so it cannot replace all Chinese output at once. Indeed, in the first year of the U.S.–China trade war, U.S. importers could not fully find alternatives for all Chinese goods, resulting in a net import decline and some unmet demand. However, given a multi-year horizon and the proactive reorientation of supply chains, the U.S. can realistically diversify many import categories away from any single adversarial source. The trade diversion in 2019 is instructive: U.S. imports from China fell by $87 billion, but imports from Vietnam, Taiwan, Mexico, and Europe rose by a combined ~$70 billion, offsetting much of the drop. This indicates a substantial ability to “reshuffle” trade flows to friendly nations. Bilateral and regional trade agreements could facilitate this process. (The U.S. already has free trade agreements with 20 countries, and could pursue new deals with emerging partners like India or African nations to secure alternative suppliers.) Over 2025–2030, one could expect the U.S. to deepen ties with countries such as Mexico, Canada (via USMCA), Vietnam, India, Taiwan, and others, creating a more tariff-resilient import network.

Figure: Change in U.S. merchandise trade with major partners (2019 vs 2018) during a tariff escalation. Imports from China plunged as tariffs hit (–$87 billion), while imports from other regions (Vietnam +$17.5 b, Europe +$31.2 b, Mexico +$11.6 b) surged to partially substitute Chinese goods. U.S. exports also fell due to retaliatory tariffs (especially to China –$13.7 b). This illustrates the ability – and limits – of short-term supply chain diversion in a trade war.

4. China and Europe’s Dependence on U.S. Demand

A three-way tariff war would expose the greater dependence that China and Europe have on the U.S. market relative to the U.S.’s dependence on them. The United States is the world’s largest consumer market, and access to U.S. buyers is crucial for export-oriented industries in both China and Europe.

China: The U.S. has been one of China’s top export destinations for decades. In 2023, China exported over $500 billion in goods to the United States– roughly 15% of China’s total exports. Categories like electronics, machinery, and furniture have especially high U.S. exposure. For example, the U.S. imported $127 billion of electrical and electronic equipment from China in 2024 alone. Losing access to the U.S. market would be a severe blow to China’s manufacturers, many of whom operate on thin margins and massive volumes. During the 2018–2019 trade war, when U.S. tariffs caused Chinese exports to the U.S. to drop, China managed to cushion the impact by redirecting exports to other regions – notably ASEAN countries and Europe. Chinese exports to ASEAN jumped by $38.5 billion in 2019, as China found alternative buyers for some goods. However, this strategy has limits. If simultaneously the U.S., EU, and other allies all raised barriers, China would find it much harder to compensate. Its domestic market, while large, cannot yet absorb the output that the U.S. and EU currently purchase. Many Chinese industries (from electronics assembly to toys to apparel) still rely on American end-consumers to sustain scale. Furthermore, China’s economic structure is still investment- and export-heavy – household consumption is only ~38–40% of China’s GDP (compared to 60–70% in the U.S.). This means China depends on external demand to a much greater degree to keep factories running. A collapse in exports due to tariffs would thus ripple through Chinese employment and growth far more intensely.

Europe (EU) and Germany: Europe as a whole exports heavily to the U.S. market, and no country more so than Germany, Europe’s export powerhouse. The U.S. is Germany’s single largest export market – in 2023 Germany sold €158 billion of goods to the U.S., nearly 10% of Germany’s total exports. The German economy, in particular, is vulnerable because of its specialization in autos, machinery, and chemicals – sectors with big U.S. customers. German automakers rely substantially on American buyers: about 13% of all German passenger cars exported are sold in the U.S., the largest share for any country. High-end German brands (BMW, Mercedes-Benz, Volkswagen’s Audi/Porsche) earn a significant portion of their profits in the U.S. luxury auto market. If U.S. tariffs make German cars more expensive, German manufacturers stand to lose market share that they might not easily recapture, given competition from U.S. and Asian brands. Beyond autos, Europe’s capital goods and aerospace industries (e.g. Airbus, industrial machinery firms) count the U.S. as a critical buyer for their jets and equipment. This reliance cuts both ways: Europe needs U.S. demand to keep its export-led growth on track. EU economies like Germany, Italy, and Ireland also have strong trade ties in pharmaceuticals and medical devices – for instance, a large share of advanced drugs and medical equipment produced in Europe is ultimately sold in America.

Other sectors (Luxury Goods, Pharmaceuticals): The U.S. market’s importance extends to less obvious areas like luxury consumer goods and pharma, which are key exports for Europe (and to some extent China for luxury). American consumers account for roughly 20–25% of global luxury goods sales【44†L31-L39】, making them vital for European luxury houses (French, Italian brands, etc.) and even high-end Chinese manufacturers. A trade war dampening U.S. demand would directly hurt luxury exporters. In pharmaceuticals, the U.S. is by far the largest single-country market – North America makes up ~45% of global pharmaceutical revenue. European pharma companies (in Germany, Switzerland, UK, etc.) depend on U.S. sales for a huge share of their income, given higher U.S. drug prices and consumption. Any barriers to U.S. pharma imports (even if unlikely due to critical needs) would leave European drug makers scrambling, as no other market matches the U.S. in scale or profitability.

In short, China and Europe have more to lose in a full-blown tariff war because their economic engines rely on selling into the U.S. market. This dependence is structural: China’s growth, and Germany’s in particular, has been fueled by net exports. By contrast, the U.S. economy is driven primarily by domestic demand – making it comparatively less vulnerable to losing foreign markets.

5. Why the U.S. Holds the Upper Hand in a Tariff Escalation

Bringing the above points together, the United States possesses several strategic advantages in an escalating global tariff war:

Unmatched Purchasing Power: The U.S. consumer market is the world’s largest, giving the U.S. considerable leverage. Exporters in China and Europe cannot easily replace the American buyer. As one observer put it, “The United States is the largest consumer market in the world. Shutting [U.S. consumers] out will impact your bottom line.” This means other countries have a strong incentive to maintain access to U.S. markets, whereas the U.S. can endure some loss of export markets. No other economy can readily absorb the volume of goods that the U.S. imports; for example, if Chinese firms are shut out of the U.S., finding equivalent demand in Europe or domestically would be extremely difficult.

Resilience to Export Shocks: Because exports are a relatively small fraction of U.S. GDP (about 11–12%), the U.S. can weather retaliatory tariffs with less macroeconomic damage. A decline in exports hurts particular industries (like agriculture or aircraft manufacturing), but overall U.S. growth is not derailed. In the last trade war round, U.S. exports did fall (U.S. goods exports to China were down ~$14 billion in 2019 due to retaliation), yet the U.S. economy continued growing on the back of domestic consumption. By contrast, export-reliant economies risk recession if major export markets are cut off. This asymmetry means tariff escalation inflicts relatively more pain on China and Europe (in terms of lost GDP percentage) than on the U.S.. The U.S. also has fiscal and monetary capacity to buffer its producers (through subsidies or stimulus) if export industries suffer, as seen with aid to farmers during the China trade war.

Figure: Export dependence of the U.S. versus major economies. The U.S. exports only ~12% of its GDP, compared to ~20% for China and ~47% for Germany. This lower reliance on exports implies the U.S. economy is less vulnerable to losing foreign market access in a trade war.

Ability to Reshape Supply Chains: The U.S. and its companies have demonstrated an ability to redirect supply chains in response to tariffs. With its considerable import volumes, the U.S. can incentivize other countries to scale up production and step into any gaps left by China or Europe. We have already seen supply-chain migration to Southeast Asia, Mexico, and other regions when tariffs made Chinese goods costlier. Over a longer horizon (2025–2030), the U.S. can actively foster alternate suppliers. Trade policy can support this – for instance, through new bilateral trade agreements or investment deals with countries like Vietnam, India, or African nations that offer manufacturing capacity. By spreading its import demand among a wider base of partners, the U.S. reduces any one country’s chokehold on its supply. This flexibility is a strategic asset: while China cannot easily find a second United States as an export customer, the U.S. can find multiple “small Chinas” to source from (each providing a slice of what China used to, even if none alone matches China’s scale). Additionally, U.S. firms can reshore certain production where feasible, further enhancing flexibility.

Alliances and Coordinated Pressure: In a scenario where Europe joins the U.S. in raising tariffs against China, China’s position becomes more precarious. The U.S. can coordinate with allies (EU, Japan, Canada, etc.) to form a united front in trade disputes. Collectively, the developed markets form the majority of global high-value consumption – meaning export-dependent nations have nowhere to turn if shut out of all these markets simultaneously. This coordinated leverage is a strength for the U.S. side (assuming transatlantic alignment), effectively boxing in rivals like China. Even if Europe is also in a trade tiff with the U.S., the U.S. could still leverage one-on-one deals – for example, a trade understanding with the UK or others to keep certain supply lines open, while isolating adversaries. The dollar’s dominance and U.S. financial power also amplify trade leverage (though indirectly), as many countries need access to U.S. financial markets and the dollar system, giving the U.S. additional tools (sanctions, etc.) to enforce trade objectives.

Structural Weaknesses Abroad: China and Germany (and similar export-led economies) face structural economic weaknesses that reduce their leverage. China is already grappling with slower growth, high corporate debt, and a necessary rebalancing toward domestic consumption. A tariff war exacerbates China’s challenges, potentially accelerating capital flight or supply chain decoupling that was already underway. Germany and other European exporters are simultaneously dealing with aging populations, high energy costs, and post-pandemic demand shifts; a loss of U.S. sales could tip some into stagnation.

In essence, countries like China and Germany need trade surpluses for growth a strategic vulnerability. The U.S., with a large services sector and innovative tech economy, is less structurally dependent on manufacturing exports. This doesn’t mean the U.S. is invulnerable (certain regions and industries would suffer), but at a national level the U.S. can absorb the shock more robustly than its rivals.

6. How a Tariff War Could Positively Impact Bitcoin

In the context of escalating global tariff conflicts, Bitcoin could experience significant positive impacts, functioning as a financial safe haven and an alternative to traditional economic systems disrupted by tariffs.

Safe-Haven Asset Appeal: In times of geopolitical uncertainty and economic instability, investors typically seek safe-haven assets like gold and government bonds. Increasingly, Bitcoin is viewed as a "digital gold" due to its decentralized nature, limited supply, and independence from government interference. A prolonged tariff war, causing volatility in traditional markets, could drive investors toward Bitcoin as a hedge against inflation, currency devaluation, and economic downturns.

Increased Cross-Border Transactions: Tariffs typically lead to higher transaction costs and economic frictions in international trade, as traditional banking systems grapple with regulatory complexities. Bitcoin, being borderless and free from traditional banking constraints, offers an attractive alternative for businesses and individuals seeking more efficient cross-border payments. This could significantly boost Bitcoin adoption as traders and companies circumvent restrictive tariff regimes and traditional banking barriers.

Currency Devaluation and Bitcoin Adoption: Countries adversely impacted by tariffs may see their currencies weaken significantly. A weakening fiat currency can prompt individuals and businesses to diversify into more stable and internationally accepted stores of value, such as Bitcoin. Historical precedents, like currency crises in Argentina and Turkey, have shown Bitcoin adoption surges during periods of significant currency depreciation.

Decentralization and Financial Autonomy: Tariff wars often lead to increased government controls and tighter regulatory measures on traditional financial systems. Bitcoin’s decentralized nature offers an appealing counterbalance to government-controlled fiat currencies. Citizens in economies with stringent capital controls or government interventions could turn increasingly toward Bitcoin, appreciating its censorship resistance and autonomy.

Trade Settlement of Energy: As a sign of things to come and a major shift away from the U.S. dollar as the world’s reserve currency, Russia and China are increasingly settling oil trades in Bitcoin—bypassing Western sanctions and validating BTC as a tool for cross-border commerce and sovereign transactions.

In summary, a global tariff war scenario could significantly bolster Bitcoin's adoption and valuation, positioning it as a preferred financial instrument for stability, efficiency, and independence in an otherwise uncertain economic landscape. In conclusion, an escalating tariff war among the U.S., China, and Europe would impose economic costs all around, but the distribution of pain would be uneven. The U.S. – by virtue of its massive internal market, lower trade dependence, and adaptable import sourcing – is comparatively well positioned to endure and even prevail in a prolonged trade confrontation. Low foreign tariffs have historically contributed only marginally to U.S. GDP, whereas foreign economies rely greatly on American markets for growth. The initial pain of tariffs (higher prices) for the U.S. is real, but manageable and likely temporary as supply chains adjust. Meanwhile, China and export-centric European economies would face a more daunting challenge: they would be pressured to reinvent their growth models if cut off from the American consumer. This dynamic suggests that, as risky as trade wars can be, the side with the deeper pockets and bigger home market – in this case, the United States – holds a stronger hand in the “game” of tariff escalation.

Erasmus Cromwell-Smith

April 7th, 2025.

https://medium.com/@e-cromwellsmith

Sources:

U.S. Bureau of Economic Analysis; World Bank; Cato Institute; WITA; USCIB Foundation; American Affairs (Trevor Jones); VanEck - https://www.vaneck.com/us/en/blogs/investment-outlook/our-portfolio-managers-weigh-impact-of-trumps-tariffs/#digital-assets-bitcoin