The Case for David Bailey's $710 Million Bitcoin Treasury Vehicle

The KindlyMD–Nakamoto Holdings Merger: In-Depth Analysis

Research Brief

On May 12, 2025, KindlyMD, Inc. (NASDAQ: KDLY) – a Utah-based healthcare services provider – announced a definitive merger agreement with Nakamoto Holdings, Inc., a newly formed Bitcoin-focused holding company founded by David Bailey. The deal transforms KindlyMD into a publicly traded Bitcoin treasury vehicle, marking a radical shift from its healthcare roots. Key details of the merger structure include:

Capital Raise: The transaction is accompanied by a massive $710 million financing package – $510 million in a PIPE (Private Investment in Public Equity) and $200 million in senior secured convertible notes. This $710M raise is touted as the largest ever capital raise to launch a Bitcoin treasury, and the $510M PIPE is the largest PIPE for any public crypto-related transaction to date. The PIPE was priced at $1.12 per KindlyMD share (with attached warrants), signaling the involvement of a large number of investors at a relatively low entry price. The $200M convertible note, maturing in 2028, was issued to a single institutional buyer (discussed below).

Public Listing via Merger: By merging with KindlyMD (already listed on Nasdaq under KDLY), Nakamoto Holdings gains an immediate Nasdaq listing for the combined entity. Shares of KindlyMD spiked dramatically on the announcement as the market digested the new Bitcoin-focused strategy. KindlyMD’s stock will continue to trade as “KDLY” until the merger closes, after which a new company name and ticker will be adopted. This reverse-merger approach (using an existing Nasdaq-listed company) provides a faster route to public markets than a traditional IPO, giving the new venture a compliant, transparent public structure for Bitcoin exposure from day one.

Strategic Intent – Bitcoin Treasury Vehicle: The combined company’s core mission is to accumulate Bitcoin and increase the Bitcoin held per share (“Bitcoin Yield”) over time. In effect, the firm is positioning itself as a Bitcoin treasury holding company, similar to a publicly traded Bitcoin fund but with an operating business attached. The strategy will use equity, debt, and other financial offerings to raise capital and purchase more BTC, thereby growing the treasury. According to the announcement, this structure offers public-market investors exposure to Bitcoin’s price appreciation within a compliant, transparent framework managed by experienced Bitcoin veterans. The strategic intent is explicitly long-term: management and investors share a belief in Bitcoin’s long-term value, aiming to make the company a leading public Bitcoin holding vehicle.

“Bitcoin-Native” Ecosystem Vision: Beyond just holding BTC, Nakamoto’s broader vision is to build an ecosystem of Bitcoin-native companies under its umbrella. According to the press release, this merger is the first step toward a global network of Bitcoin-focused businesses, potentially spanning media, advisory, and financial services. The combined company is partnering with one of the world’s most influential Bitcoin marketing platforms in support of this strategy. David Bailey described the merger as creating a public vehicle at the convergence of traditional finance and the Bitcoin market: “Traditional finance and Bitcoin-native markets are converging. The securitization of Bitcoin will redraw the world’s economic map,” he stated, emphasizing a future where “every balance sheet – public or private – holds Bitcoin.” By packaging Bitcoin into familiar instruments (equities, debt, preferred shares, etc.), the company aims to bring Bitcoin to the center of global capital markets. In Bailey’s words, “Our mission is simple: list these instruments on every major exchange in the world.”

Nasdaq Listing Implications: Being listed on Nasdaq confers additional credibility and liquidity to the venture. It allows institutional investors who may not hold cryptocurrencies directly to get exposure via a traditional stock ticker. This structure parallels the approach pioneered by MicroStrategy in 2020 (which repurposed its public stock as a Bitcoin proxy), but on a larger initial scale. Notably, the company claims it will be a leading public market Bitcoin treasury from inception, providing a new vehicle for investors to bet on Bitcoin’s appreciation through the equity markets. The listing also imposes regulatory transparency (SEC filings, audits, etc.), which could appeal to investors who demand more oversight than a private crypto fund provides.

In summary, the KindlyMD–Nakamoto deal creates a publicly traded Bitcoin holding company overnight. With $710 million in fresh capital, the new entity is poised to start accumulating a substantial Bitcoin reserve, effectively converting KindlyMD from a healthcare firm into a Bitcoin treasury and investment conglomerate. The strategic intent is not just to hold BTC, but to grow a whole ecosystem around Bitcoin, leveraging public markets and regulatory compliance to normalize Bitcoin as a treasury asset.

Leadership: David Bailey’s Role and Political Influence

The driving force behind this merger is David Bailey, who will become the CEO of the combined company. Bailey is a well-known figure in the Bitcoin ecosystem, bringing both industry experience and unique political connections to the venture:

Bitcoin Industry Background: David Bailey is the founder of BTC Inc., the parent company of Bitcoin Magazine (one of the oldest and most influential Bitcoin publications) and organizer of the annual Bitcoin Conference. He is also General Partner of UTXO Management, a Bitcoin-focused investment firm. Under his leadership, BTC Inc. built industry-leading platforms at the heart of the Bitcoin ecosystem – for instance, Bitcoin Magazine and its events have become central hubs for the Bitcoin community. This background gives Bailey deep credibility and connections in the crypto industry. His team is described as a seasoned management group with decades of Bitcoin experience, indicating that veteran Bitcoiners will be at the helm of the new company. By installing Bailey as CEO, the merged company signals that it will be led by Bitcoin natives who understand the technology, the culture, and the long-term vision of “hyperbitcoinization.”

Strategic Leadership of the Combined Company: Bailey’s role as CEO means he will steer both the capital allocation (Bitcoin treasury strategy) and the expansion into ancillary Bitcoin businesses. The merger agreement also brings over a marketing services arrangement, meaning a major media company will actively promote and support the Bitcoin treasury strategy. The Board of Directors is slated to include six appointees from Nakamoto versus one from KindlyMD, giving Bailey and his team effective control over strategic decisions. In essence, Bailey is using KindlyMD as a vehicle to reverse-merge his vision of a Bitcoin holding conglomerate into the public markets, with himself in the driver’s seat.

Political Influence – Advising Donald on Bitcoin: Uniquely, David Bailey has leveraged his Bitcoin influence into the political realm. He served as an advisor to Donald Trump on crypto policy during Trump’s 2024 presidential campaign. This connection proved to be quite consequential: during the 2016–2020 period, Trump had been openly hostile to Bitcoin. However, in the 2024 campaign, Trump’s stance changed to overtly pro-Bitcoin – a shift that coincided with Bailey’s advisory role. In May 2024, Trump announced that he was “pro-Bitcoin” after years of dismissing it. This was a remarkable about-face and signaled that pro-crypto voices (like Bailey) had gained Trump’s ear.

Trump’s Pro-Bitcoin Rhetoric and Bailey’s Messaging: There are clear signs that Bailey’s messaging and the Bitcoin community’s priorities were reflected in Trump’s campaign rhetoric. At the high-profile Bitcoin 2024 conference in Nashville – organized by BTC Inc. – Donald Trump was a keynote speaker, an unprecedented appearance for a major presidential candidate at a crypto event. Bailey, as the conference host, introduced Trump to a packed arena of Bitcoin enthusiasts. In his speech, Trump catered directly to Bitcoiners. He pledged, “On day one, I will fire Gary Gensler,” referring to the crypto-skeptical SEC Chairman – a line that brought the crowd to its feet in a standing ovation. This promise aligned perfectly with grievances of the Bitcoin community. Trump also vowed to oppose a central bank digital currency (CBDC) and uphold the right to self-custody of Bitcoin, and he talked about making the U.S. “the Bitcoin superpower of the world” by encouraging Bitcoin mining domestically. All of these talking points – from firing regulators seen as anti-crypto, to anti-CBDC stance, to framing Bitcoin as aligned with American prosperity – mirror the advocacy of prominent Bitcoin proponents like Bailey. It’s evident that Bailey and his peers successfully impressed upon Trump the political upside of embracing Bitcoin.

Post-Election Reflections: By early 2025, following the 2024 election, Donald Trump’s engagement with Bitcoin did not stop at campaign rhetoric. Trump won the 2024 election, making him President again in January 2025. In the initial months of 2025, the new administration’s policy direction showed signs of the promised crypto-friendliness. While concrete actions take time, the tone from the White House was notably warmer towards Bitcoin than in Trump’s first term. The influence of Bailey’s advisory can be seen in the administration’s early statements – for instance, there were discussions about rolling back certain regulatory pressures on crypto businesses and exploring tax incentives for Bitcoin mining on U.S. soil. Trump’s public call-out of Gensler at the Bitcoin conference was a clear signal. In short, Bailey’s role as a bridge between the Bitcoin community and top political figures helped inject Bitcoin-friendly ideas into the highest levels of policy discourse. This could pay dividends for the KindlyMD–Nakamoto venture as well, since a friendlier regulatory environment and broader political acceptance of Bitcoin would directly benefit a Bitcoin treasury company. Bailey’s dual identity – Bitcoin entrepreneur and informal political strategist – uniquely positions him to champion pro-Bitcoin policies that may enhance the long-term viability of his business strategy.

In summary, David Bailey not only brings industry expertise to the CEO role but also a powerful network. His leadership of Bitcoin media and events gives the new company a built-in marketing and community outreach arm, and his influence on political figures (particularly Donald Trump) suggests he can help shape an environment conducive to Bitcoin adoption. This merger is as much an investment bet on Bitcoin as it is a bet on Bailey’s ability to lead and advocate for Bitcoin at all levels of society.

Investor Consortium and Financing Breakdown

The KindlyMD–Nakamoto merger came together with the backing of an unusually large and diverse investor consortium, reflecting a mix of crypto industry pioneers, venture funds, and specialist investors. Here we provide a breakdown and assessment of the $710 million financing:

PIPE Investors ($510M): The PIPE – private investment in public equity – was the primary funding mechanism, raising $510 million. According to the company, this PIPE included over 200 investors spanning six continents, highlighting broad global interest. The PIPE was structured as KindlyMD common stock (at $1.12 per share) with attached warrants, indicating investors got equity in the post-merger company at a bargain-basement price. Such a large number of participants for a PIPE is notable; it suggests many high-net-worth individuals and family offices took part, alongside funds. The notable investors disclosed include:

Institutional Funds: Actai Ventures, Arrington Capital, BSQ Capital Partners, Kingsway Capital, Off the Chain Capital, ParaFi Capital, RK Capital, VanEck, and Yorkville Advisors. These range from crypto-focused venture firms to traditional asset managers and hybrid crypto funds. Yorkville Advisors stands out – not as a crypto VC, but as a fund known for structured PIPE deals; notably, YA II PN, Ltd., a fund managed by Yorkville, was the sole purchaser of the $200M convertible note as discussed below. The inclusion of Yorkville (both in the PIPE and leading the note) signals that a portion of the financing has a structured, possibly hedged, approach. Meanwhile, others like Kingsway and Off the Chain are crypto-centric, and VanEck is an asset manager that has pursued Bitcoin ETFs. Overall, these institutional participants are largely specialized crypto investors or opportunistic investment funds rather than household-name Wall Street banks.

Notable Individuals: The PIPE also drew contributions from prominent individuals in the crypto and tech world, such as Adam Back, Balaji Srinivasan, Danny Yang, Eric Semler, Jihan Wu, Ricardo Salinas, and Simon Gerovich. This roster reads like a who’s who of early Bitcoin and crypto entrepreneurs. Adam Back, CEO of Blockstream, is a legendary cryptographer; Balaji Srinivasan, former Coinbase CTO, is known for bold crypto predictions; Jihan Wu co-founded Bitmain, the largest Bitcoin mining equipment maker; Ricardo Salinas Pliego is a Mexican billionaire who has embraced Bitcoin; Eric Semler is the CEO of Semler Scientific; Simon Gerovich leads Metaplanet. In sum, the PIPE investor base skews towards crypto “OGs” and dedicated crypto funds, with a sprinkling of traditional investors who are crypto-friendly.

Many of these individuals likely invested their personal funds rather than via their operating companies. This underscores that, at least for this deal, the belief and funding came from the crypto community and its wealthy allies, not from big public companies adding Bitcoin to their balance sheets. It appears the financing was not overtly political; it was driven by Bitcoin-focused investors.

Convertible Notes ($200M): In addition to the PIPE, the merger financing includes $200 million in convertible notes, all of which was taken up by a single purchaser: YA II PN, Ltd. managed by Yorkville Advisors. These notes are senior secured and likely have a conversion feature into equity at a later date (maturing in 2028). Yorkville’s involvement is significant – Yorkville is known for providing financing to micro-cap public companies via structured deals. In this case, they essentially lent $200M in exchange for an instrument that can convert into the combined company’s stock. This suggests a vote of confidence in the venture’s viability from a financial engineering perspective; however, it also means Yorkville could potentially hedge or sell shares upon conversion, which might introduce selling pressure down the line. For now, though, the $200M note is an important piece of the capital structure that gave Bailey’s team additional upfront cash to deploy into Bitcoin.

Investors’ Profiles – Individuals vs Enterprises: Notably, the sources of capital here are primarily individuals and private investment funds, rather than large operating companies or cash-rich corporate treasuries. The investor list does not include any Fortune 500 corporates or major institutional asset managers in a lead role. In other words, this raise relied on private wealth and crypto-native funds more than traditional corporate money. The advantage is that it brings together many experienced Bitcoin advocates likely to be long-term HODLers of the stock, aligned with the vision of accumulating BTC. Their industry expertise could help Nakamoto find deal flow and partnerships. The challenge is the relative lack of institutional “whales.” With no single large patron, the company will need to cultivate a broad base of support and possibly return to the market for future capital raises if Bitcoin’s price remains volatile.

Plausible Ties to Trump or Political Networks: From the disclosed names, no obvious member of Trump’s inner circle or family is present. There’s no indication that Trump himself or high-profile political donors like the Mercers joined. It appears the financing was not shaped by political ties but rather by Bitcoin-focused motives. That said, some participants may have overlapping interests with pro-Bitcoin politicians, especially if the administration maintains its favorable stance.

Assessment of Investor Base: The financing of the KindlyMD–Nakamoto merger was unprecedented in size for a crypto-focused deal, fueled largely by the Bitcoin faithful – a mix of crypto venture funds and prominent early Bitcoin entrepreneurs around the world. The PIPE investors bring credibility from the crypto industry, and the convertible note from Yorkville brings a touch of Wall Street structured finance to the table. While the investor list doesn’t include household-name institutions, it does provide a strong foundation of Bitcoin-savvy capital. This base will be important for the company’s long-term support: these investors presumably understand the volatility and long-term nature of a Bitcoin treasury play and are on board with Bailey’s vision to grow a Bitcoin conglomerate.

Table 1: Selected Notable PIPE Investors in KindlyMD–Nakamoto Merger

Sources: Company press release and public investor profiles.

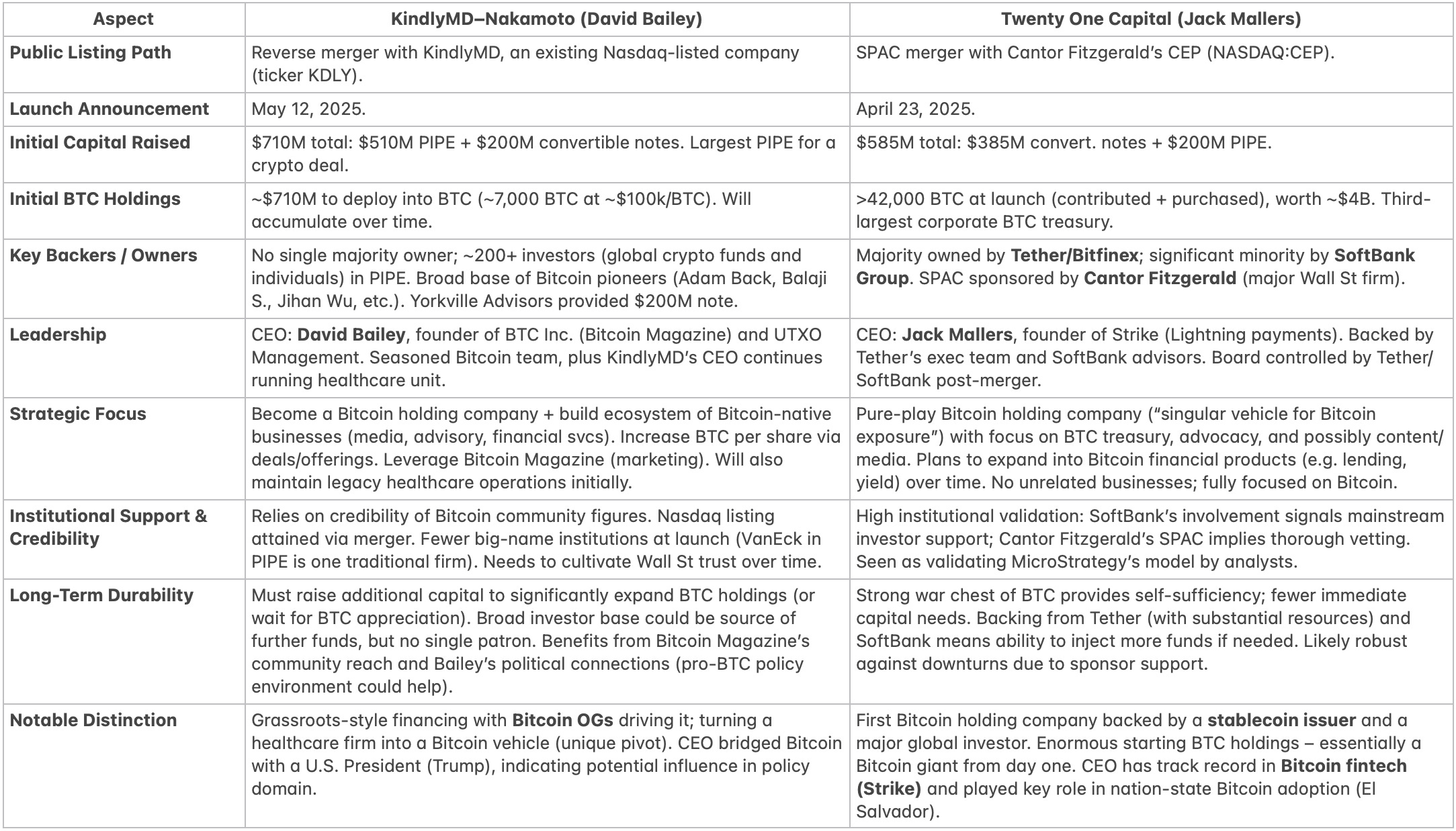

Comparison with Twenty One Capital (Jack Mallers’ Bitcoin Initiative)

The KindlyMD–Nakamoto deal invites comparison to another high-profile Bitcoin “treasury vehicle” initiative: Twenty One Capital, led by Jack Mallers (CEO of Strike). Both emerged in spring 2025 with the goal of creating large, publicly traded Bitcoin holding companies. However, they differ significantly in scale, structure, and backing. Below we contrast the two:

Formation and Structure: Twenty One Capital is being created via a merger with a special-purpose acquisition company (SPAC) called Cantor Equity Partners (CEP), sponsored by Cantor Fitzgerald. In April 2025, Tether (the largest stablecoin issuer) and SoftBank Group unveiled plans to launch Twenty One by contributing assets and capital through this SPAC deal. Jack Mallers was named co-founder and will serve as CEO of Twenty One, much as David Bailey is CEO of Nakamoto. KindlyMD–Nakamoto, in contrast, used a reverse merger with an operating company (KindlyMD) rather than a SPAC, and it did not have a single sponsor like Cantor or a pre-merger asset contribution from a strategic partner. Essentially, Twenty One is a pre-planned SPAC combination backed by major players, whereas Nakamoto is a founder-led takeover of an existing small-cap company.

Initial Bitcoin Treasury Size: Twenty One Capital’s initial Bitcoin treasury dwarfs Nakamoto’s in sheer size. Twenty One is expected to launch with over 42,000 BTC on its balance sheet, worth nearly $4 billion at prevailing prices in April 2025, making Twenty One the third-largest corporate holder of Bitcoin globally. By comparison, the $710M raised for Nakamoto, if deployed into BTC, would amount to roughly 6,500–7,500 BTC (depending on Bitcoin’s price). This is an order of magnitude smaller treasury. Even if Bitcoin’s price were lower, Nakamoto’s initial BTC holdings would still be in the single-digit thousands of coins – far below Twenty One’s 42K. In short, Mallers’ group is starting with about 5–6 times more Bitcoin in reserve than Bailey’s group. This massive difference is due largely to Twenty One’s anchor investors (Tether and SoftBank) likely contributing either cash or BTC upfront. Nakamoto’s funds will be deployed into BTC after the merger.

Capital Raised and Funding Structure: Interestingly, Bailey’s deal raised more new cash ($710M) than Twenty One did in its PIPE/notes ($585M), but Twenty One’s backers likely brought existing Bitcoin or additional private funding to reach that 42K BTC figure. Twenty One’s financing consisted of $385M in convertible notes and $200M in PIPE equity, versus Nakamoto’s $200M notes + $510M PIPE. So on paper, KindlyMD–Nakamoto secured slightly more capital from investors. However, the composition of investors differs greatly:

Twenty One Capital Backers: The cornerstone investors are Tether/Bitfinex (which will own a majority of Twenty One) and SoftBank Group (which will hold a major minority stake). Cantor Fitzgerald’s SPAC also implies traditional financial backing and due diligence. Tether’s involvement is significant – Tether has vast reserves from its stablecoin business, and by backing Twenty One, it effectively injects a portion of those resources and its institutional heft. SoftBank, a conglomerate with a global footprint, brings a stamp of mainstream credibility. In addition, Twenty One raised funds via a PIPE that likely included large institutional investors, and had Cantor Fitzgerald structuring the deal. The support of a major investment bank and multi-billion-dollar enterprises means Twenty One launched with considerable institutional support.

KindlyMD–Nakamoto Backers: As detailed, the investor base here was fragmented among many individuals and crypto funds, with no single shareholder controlling a majority post-merger. There is no equivalent of a SoftBank or Tether in Bailey’s deal. While some institutions participated, they are minority stakeholders. The closest analog is Yorkville’s role (a finance firm injecting $200M via notes), but Yorkville is not an operating company adding strategic value; it’s more of a financier. In terms of credibility, Bailey’s group leans on the reputations of Bitcoin luminaries and the community, whereas Mallers’ group can lean on the brands of Tether and SoftBank, plus Cantor Fitzgerald. This gives Twenty One an aura of institutional legitimacy and firepower that Nakamoto will have to build over time.

Leadership and Team: Both ventures are led by well-known young Bitcoin entrepreneurs:

Jack Mallers (Twenty One) is famous for founding Strike, a Bitcoin payments app, and for his role in facilitating El Salvador’s adoption of Bitcoin. Mallers has credibility as a builder of Bitcoin payment infrastructure and is seen as a rising star in the Bitcoin movement.

David Bailey (Nakamoto) brings media and community leadership experience via Bitcoin Magazine and political connections. Bailey’s strength is in strategy, advocacy, and community building, whereas Mallers’ strength is in technology integration and partnerships.

Both have complementary high-profile allies: Mallers is closely allied with people like Nayib Bukele (President of El Salvador) and Tether’s leadership, while Bailey is allied with Bitcoin OGs and the President of the United States. It’s interesting that each bridges into different spheres.

Long-Term Strategic Durability: In terms of strategy durability and credibility:

Twenty One’s Outlook: With deep-pocketed backers (Tether and SoftBank) that can channel more capital if needed, Twenty One likely has greater access to follow-on funding. Its initial BTC horde (42K) provides a huge cushion. The involvement of Cantor Fitzgerald suggests rigorous vetting, which bodes well for its internal controls and governance. One could argue Twenty One’s model is very durable: it’s essentially an alliance between the biggest stablecoin issuer and a major investment firm. On balance, analysts viewed Twenty One’s launch as a strong validation of the Bitcoin treasury concept.

KindlyMD–Nakamoto’s Outlook: Bailey’s venture starts with fewer big safety nets. Its war chest is significant ($710M), but once that is converted to ~7K BTC, the company must rely on its management acumen to grow that number. It will need to continually convince investors to provide more capital in exchange for stock or other instruments. Another aspect is Bailey’s media and political playbook: Nakamoto has at its disposal the Bitcoin Magazine platform and conferences for outreach, which could help attract retail investors and smaller institutions as shareholders. Also, because KindlyMD’s original business will continue to operate, the company retains a real operating business that generates revenue. This provides some cash flow and a human services mission. In terms of credibility, Nakamoto will need to prove itself over time.

Use of Funds and Business Focus: Both companies state a similar goal – maximize Bitcoin holdings per share – but there are nuances:

Twenty One has explicitly mentioned it will also focus on Bitcoin advocacy and content/media, and eventually Bitcoin-native financial products. It might venture into businesses like Bitcoin lending or structured products.

Nakamoto, through Bailey, has outlined a vision of an ecosystem including media, advisory, and financial services. Nakamoto may rely on its existing media platform for content and outreach rather than building its own. Over time, Nakamoto might acquire other Bitcoin businesses.

When comparing financial scale, strategic support, and credibility:

Financial Scale: Twenty One launched with a much larger Bitcoin war chest (~42K BTC vs ~7K BTC).

Strategic Durability: Twenty One’s backing by Tether/SoftBank implies it has patient, deep-pocketed shareholders. Nakamoto is more exposed to having to court the market for future capital.

Credibility & Institutional Support: Twenty One clearly wins on traditional institutional backing. Nakamoto’s credibility is strongest within the Bitcoin community.

They are not necessarily adversarial – they might both thrive. Each provides a slightly different vehicle for investors: Twenty One is more institutional in profile, Nakamoto more grassroots with a wider base of Bitcoin pioneers. Time will tell which model proves more effective.

Table 2: KindlyMD–Nakamoto vs. Twenty One Capital – Key Comparison

Sources: Press releases and news coverage

Future Outlook: Prospects for Replicating Such Mega-Deals

The emergence of these mega-deals – KindlyMD–Nakamoto’s $710M raise and Twenty One Capital’s Bitcoin infusion – begs the question: will we see more large-scale Bitcoin treasury vehicles in the future, and who will fund them? A few points stand out:

High-Water Mark for Bitcoin Treasuries: The bar has been set high. Twenty One’s >42,000 BTC and Nakamoto’s ~$710M war chest represent a new high-water mark for publicly disclosed Bitcoin acquisitions. To match or exceed these, future entities would need to marshal hundreds of millions – if not billions – of dollars dedicated to buying Bitcoin. The universe of investors capable of writing such large checks is relatively small.

From Crypto Insiders to Institutional Capital: The KindlyMD–Nakamoto deal leaned on crypto insiders and entrepreneurs; Twenty One brought in a large private crypto company (Tether) and a major public company (SoftBank). As the space matures, the next wave might involve even more traditional capital:

Large Enterprises with Cash Flow: We may see profitable firms decide to allocate a portion of their treasuries to Bitcoin or spin up holding subsidiaries.

Sovereign Wealth Funds (SWFs): SWFs (such as those in the Middle East or Asia) have the financial firepower to deploy billions into assets like Bitcoin. Some already tested crypto investments; a move into direct BTC allocations would be a leap, but plausible as Bitcoin matures.

Institutionalization and Mainstream Interest: Each successive deal lowers the perceived risk for the next, by providing proof of concept. MicroStrategy’s move in 2020 was the first domino. By 2025, multiple public companies explicitly dedicated to holding Bitcoin have emerged. As more do so, they validate the concept and attract attention from bigger investors. We may soon see dedicated Bitcoin holding companies become an accepted category of investment, akin to REITs.

Need for Massive BTC Treasuries: One reason future deals may need large backers is the increasing scale required to make a splash. Acquiring tens of thousands of BTC is not trivial, requiring either extended OTC accumulation or buying from existing large holders. Some whales or crypto firms might roll their holdings into a public vehicle for liquidity.

Dependence on Market Conditions: The feasibility of replicating these mega-deals also depends on the Bitcoin market and macro environment. In a bull market, raising $500M+ for Bitcoin exposure is easier; in a bear market, it becomes challenging.

Regulatory and Political Support: A pro-Bitcoin stance in Washington could make it easier to launch Bitcoin financial vehicles. If spot Bitcoin ETFs are approved, some capital might flow there instead of corporate treasuries. Meanwhile, new deals could involve direct alliances with national governments or state investment funds.

In conclusion, future mega-deals akin to KindlyMD–Nakamoto and Twenty One Capital are certainly conceivable, but they will likely require the involvement of players with even deeper pockets. The initial wave tapped the low-hanging fruit of crypto insiders and forward-thinking funds. The next wave may need to pull in large-cap corporations, major financial institutions, or sovereign entities to reach new heights. As Bitcoin matures, we see increasing convergence between crypto and traditional finance. It’s reasonable to expect that large enterprise balance sheets and sovereign wealth will become the next sources of capital for Bitcoin treasuries, especially as the asset class proves itself. If Bailey’s vision holds true, today’s $700M–$800M deals could look small in hindsight. However, practical considerations (like volatility and regulation) will temper the pace. We might first see incremental growth before the next giant leap. One thing is clear: the KindlyMD–Nakamoto merger and the Twenty One launch have established a template. They show that if you gather the right coalition of investors, you can create a publicly traded Bitcoin vehicle at scale. The door is now open for more entrants, and with Bitcoin’s mainstream credibility improving, the magnitude of capital raises will likely trend upward.

Erasmus Cromwell-Smith

May 2025.

Sources:

KindlyMD–Nakamoto merger press release, Business Wire (May 12, 2025).

Nasdaq/Bitcoin Magazine report on the merger (May 12, 2025).

CoinDesk coverage of David Bailey’s plans and background (May 2025).

Cointelegraph news on the merger (May 12, 2025).

Guardian report on Trump’s Bitcoin 2024 conference speech (July 31, 2024).

Business Wire press release on Twenty One Capital (Apr 23, 2025).

CoinDesk analysis of Twenty One vs MicroStrategy (Apr 24, 2025).

The Global Treasurer analysis of the Nakamoto deal (May 13, 2025).