Limitless: The Ceiling Doesn't Exist

“In practice, the debt limit has no impact on government spending”

- Congressman Bill Foster

On January 20, 2023, Congressman Bill Foster introduced bill H.R.415, also known as "the End the Threat of Default Act." This bill proposes to eliminate the US government's debt limit. If passed, it has the potential to have a significant impact on the "full faith and credit" of the US government. Many would argue that in practice there is no debt ceiling because it has been raised 78 times since 1960. However the complete elimination of the debt ceiling would likely further damage the image of fiscal responsibility the US holds over other nations who spend more irresponsibly. The house of cards that is the US dollar is maintained by nothing more than trust in the system, without it the whole house can come crashing down in short order.

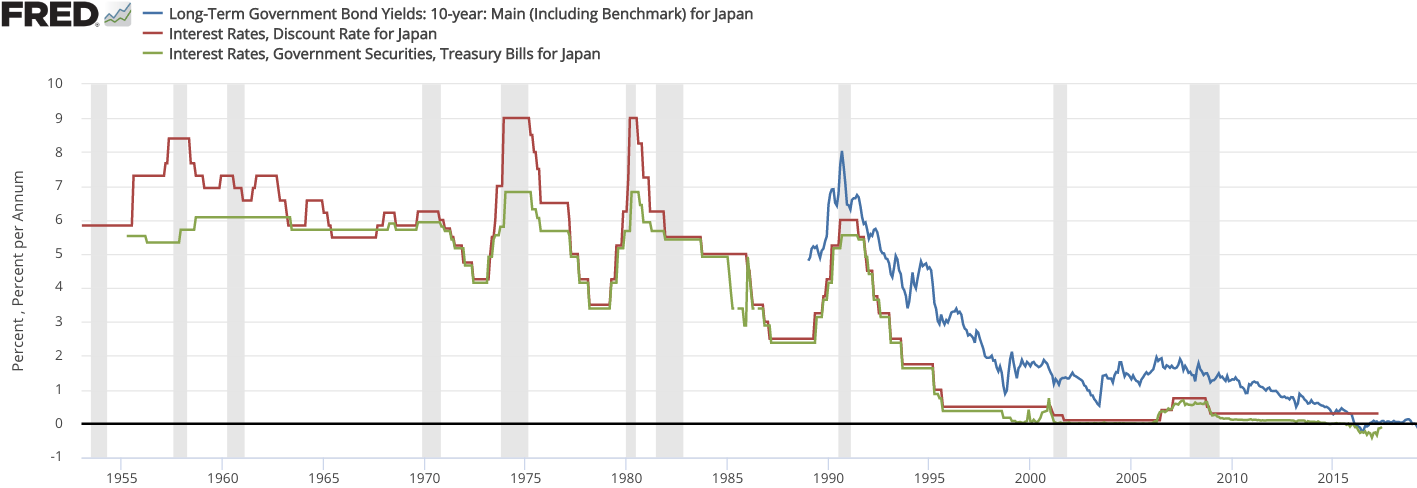

One only has to look at Japan for an example of how unlimited borrowing is likely to play out in the US.

When stagnation set in in the late 1980s the Japanese government started to intervene in the Japanese economy directly. Interest rates were lowered from 5% in 1985 to 2.5% in 1987, this led to an asset bubble in Japan. Many Japanese investors used cheap borrowing to invest in assets in other Asian countries. However, when the Bank of Japan raised interest rates from 2.5% to 6% in 1989 and 1990 the bubble burst and economic growth slowed significantly. In an effort to revive the economy, Japan implemented nine different stimulus packages during the 1990s, totaling 130 trillion yen, or roughly 1.3 trillion dollars. However, these measures did not lead to recovery. Despite the stagnation, consumer prices in Japan actually rose steadily until 1995. Beyond this point, the Japanese stimulus stopped having any meaningful impact on the economy.

In the late 1990s Japanese banks wrote off more than 50 trillion yen in bad loans.

The BOJ intervened and bought trillions of yen in commercial debt between October 1997 and October 1998. Even with this massive intervention growth remained slow, so following the advice of economist Paul Krugman the BOJ increased its asset purchases. Japanese banks received an additional 35.5 trillion yen in “liquidity injections” (printed money) between 2001 and 2004. The bank also purchased long-term government bonds to lower the yields on Japanese debt.

Economic growth appeared to return between 2002 and 2007. However, like much of the world, the country's growth slowed during the Great Recession. The Bank of Japan (BOJ) launched a new round of QE but more than 80 trillion yen in purchases was not enough. In 2014, the BOJ announced a second round of QE. This led to an increase in Japanese stocks of 30% in the following months, but there was still little indication of actual growth beyond that. As a result, in January 2016, the BOJ announced negative interest rates as a last resort measure to try to stimulate the economy.

During this entire 30 year period investors have continuously pulled out of Japan.

Specifically they have unloaded Japanese government bonds because even though they always get paid back in nominal terms, investors understand that buying and holding a Japanese bond is guaranteed to lose them purchasing power in real terms if they hold it for its full duration.

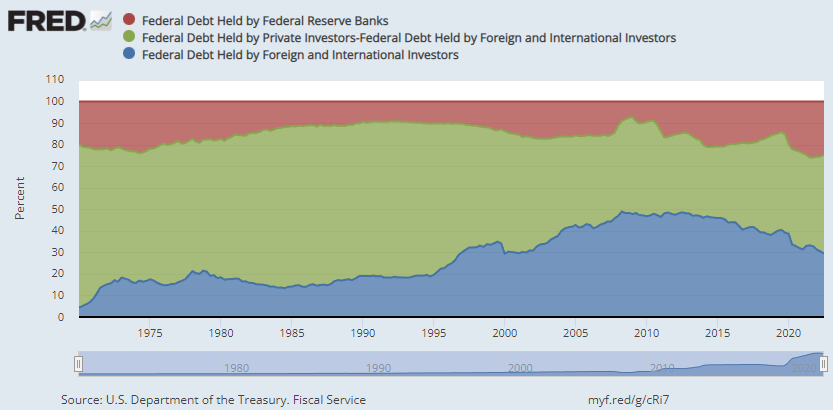

This has already begun to play out in the US as Foreign and International investors holdings of US treasuries rolled over post financial crisis.

Post 2008 financial crisis Foreign and international investors purchases of US debt rolled over. That leaves private investors and the Fed to make up the difference. It is highly likely given recent history that the difference will come mostly from the Fed because the interest rates offered on bonds are lower than the rate of inflation. This means investors are likely to seek alternatives to protect their purchasing power and will continue to reduce their purchase of US treasuries.

If Treasury yields spike due to a debt crisis, the Fed may be trapped as they cannot raise interest rates without exacerbating the crisis, but if they don't, hyperinflation may occur. This is why the Fed had to raise rates in 2022, if they didn’t their reputation would likely have suffered irreparable damage. The challenge they face now is that by raising interest rates they make the already large US government debt obligations even larger which leads to the US hitting its debt ceilings even faster. This is likely why representatives like Bill Foster want to eliminate the ceiling all together.

As the volatility in this system increases the need to remove barriers to borrowing to keep the charade going. As mentioned above, the challenge they face is that this undermines trust in the system and drives people away from it and into other systems that better protect their purchasing power.

Bitcoin is the mathematically certain lifeboat in a stormy sea of traditional finance

It provides a secure and reliable means of preserving wealth to navigate the uncertain economic conditions that lie ahead of us all. It has no debt ceiling to raise, no need for a bank to bail it out, it simply chugs along one block at a time in spite of the noise around it plucking distressed people from the murky waters below.

Thank you for reading! If you enjoyed this piece please check me out at