Automated Banking, With Bitcoin: PART THREE

PART THREE - UNLIMITED BANK TOKEN SUPPLY, AND FIXED BITCOIN TOKEN SUPPLY

The following is an ongoing series we are calling Automated Banking, With Bitcoin. The aim of this series is to offer a clear and full picture of Bitcoin for all ages and levels of adoption from nocoiner, to precoiner, to remnant pleb, in the context of fiat, and with an eye towards the inevitable outcome currently in progress. We hope you take the time to share and discuss this series as it unfolds with family and friends.

Enjoy.

PARTS ONE AND TWO RECAP

In Part One we summarized the automated financial statement preparation and automated auditability of Bitcoins ledger, removing the cost of human accountants and perhaps equally important removing the costs associated with those humans who either intentionally or inadvertently misstate those financial statements that inevitably results in investor loss of confidence business implosions and devastating unemployment spikes.

In Part Two we arrived at the realization that it is Bitcoins fixed supply that keeps Bitcoins ledger immutable and therefore allows for such high fidelity in it’s ability to record all financial transactions of bitcoin that are the basis of those automated financials.

In Part Three we are going to take a closer look at the fixed bitcoin monetary supply and contrast it with the unlimited fiat monetary supply. We will need to return to our modern banking system to learn how the system currently works, in order to then see the incredible leap of innovation that Bitcoin offers in this respect. Buckle up, we’re about to take a mind blowing journey into the world of make believe, where everyone’s money actually lives.

THE TIMES 03/JAN/2009 CHANCELOR ON BRINK OF SECOND BAILOUT FOR BANKS

From the inception of the Federal Reserve Bank of the United States of America in 1913, to 2008, the assets held by the bank gradually increased from $0 to approximately $1 trillion dollars.

But then something happened. Something very unusual. So unusual, that the Federal Reserve data, referred to as FRED, had to change all of its record keeping. To get all of the data from 1913 to present, 2023, you need to pull together two charts. Here is the second chart, 2004 to present, indicating that same balance on September 10, 2008 of approximately $1 trillion dollars, for reference.

By 2019, before more unusual stuff happened, from 2009, in the span of ten years, the balance sheet of the Federal Reserve Bank increased from $1 trillion to $4 trillion. In other words, it took the Federal Reserve Bank about 100 years to grow its assets from $0 to $1 trillion. And then somehow, the Bank grew its assets by $3 trillion more, not in the span of three hundred more years, as historical growth rates would suggest, but instead, within the eye watering span of ten years. And if that wasn’t enough from 2020 to 2022 the value of the banks assets doubled from $4 trillion to over $8 trillion. Not in four hundred years, as history would suggest, but in less than two years.

How could this be?

Are these accounting errors?

Where could all of this money have come from to pay for all of these assets?

According to the Federal Reserve Bank, in their own words:

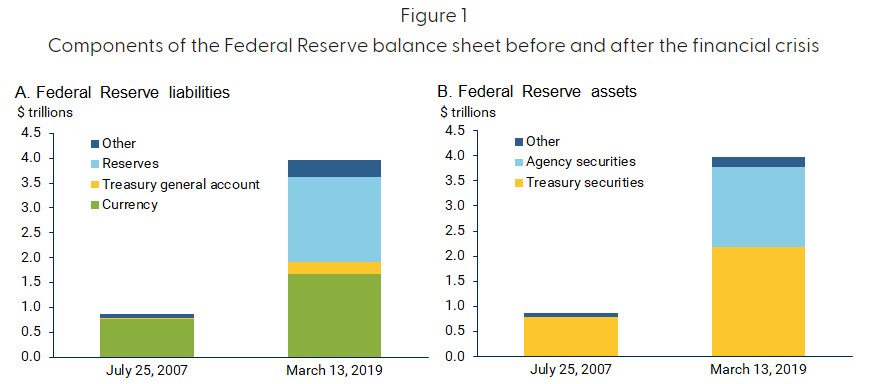

This picture has changed substantively since 2007. The right-hand bars in the two panels of Figure 1 show the balance sheet as of March, 2019. First, the size more than quadrupled to about $3.9 trillion, or about 18.5% of GDP. In contrast to the period before the financial crisis, bank reserves now constitute over 40% of Fed liabilities, about as much as currency in circulation.

This change was largely triggered by the response to the financial crisis, the Great Recession, and the ensuing slow recovery. As economic activity weakened in 2007 and 2008, the Federal Open Market Committee (FOMC) lowered the federal funds rate, the overnight interest rate that it targets to steer the economy, to essentially zero.

As the economy continued to weaken and with financial markets impaired, the Fed started buying longer-term assets, such as 10-year bonds from the Treasury and mortgage-backed securities from government agencies.

To pay for these assets, the Fed credited the accounts of the sellers’ banks at the Fed, thus increasing those banks’ reserves.

Did you hear it?

They said the quite part out loud.

Let me repeat that last line for everyone;

TO PAY FOR THESE ASSETS, THE FED CREDITED THE ACCOUNTS OF THE SELLER’S BANKS AT THE FED, THUS INCREASING THOSE BANK’S RESERVES.

Yes, that’s right, they simply created the money from nothing to buy the worthless government debts and toxic banker mortgages and bad corporate debts held by the banks.

In other words, banks made bad investments with governments, businesses and individuals, and the central bank, the Federal Reserve Bank, bought the worthless assets with money they created out of nothing by crediting an account on a computer.

With a key stroke they created the equivalent amount of money that would otherwise take hundreds of years of work to accumulate.

Still don’t believe it?

Here is Federal Reserve Chairman Ben Bernanke who oversaw the 2008 banker bailouts explaining their money printing process:

Still don’t believe it?

No problem, here is the current Federal Reserve Chairman Jerome Powell explaining the same thing for his corporate bailouts of the 2020’s:

Notice he said they print the money digitally. What does that even mean? How much of these reserves can they digitally make? Surely these people have a limited amount of money, or “bank reserves” they can create. I mean, obviously when they print this money, they are not also printing an equivalent amount of goods and services that money can buy, so obviously this monetary inflation creates price inflation.

Surely there is a limited amount this central bank plans on creating, right?

Bad news, campers. Here is Federal Reserve President Neel Kashkari explaining how much money they are able to print and that they plan to print:

So apparently the Federal Reserve Bank is simply going to keep printing reserves to bail out the banks, forever, Laura, at our expense in the form of higher housing food and energy costs. Fantastic.

Joseph Salerno, Professor Emeritus of Economics at Pace University and Academic Vice President of the Ludwig von Mises Institute provides us with the appropriate color of the Federal Reserve, referring to the organization as the Mordor of our banking system:

ITS ALL JUST A BUNCH OF TEXT MESSAGES

Ok, so the central banks create reserves out of nothing, but surely the rest of the banks in the system have actual real money, right?!

Lol, my poor sweet innocent child. No, they don’t.

Lyn Alden explained it well in her March 2023 Newsletter:

Banks currently have just $3 trillion in cash to back up their $17.6 trillion in deposits. The majority of this cash is just a ledger entry with the U.S. Federal Reserve, and so it is not tangible. Somewhere around $100 billion of it ($0.1 trillion) is held by banks in the form of actual physical banknotes in vaults and ATMs. So, the $17.6 trillion in deposits are backed up by just $3 trillion in cash, of which perhaps $0.1 trillion is physical cash. The rest is backed up by less liquid securities and loans.

In other words, the $100 dollars in your bank is actually made up of 10 cents of physical cash, $20 dollars of federal reserve balances and the remaining $79 dollars and 90 cents is made up of government debt and real estate mortgages and corporate debt that they would need to sell in order to give you your hundred dollars back.

But again, they only have 10 cents of physical money. This is why if you ask for a large amount of cash, the banks generally try not to give it to you, because if only a few people walked in on the same day to get cash, they would stop cash withdrawals. This isn’t just a Lebanon problem, this is a global banking problem, including the United States. All of the banks are tied together.

If instead you wanted to wire your $100 dollars to another bank account, your bank would be much more willing to do this, but here as well, there is usually some delays in this process, and for the same reason, because if a few more people than usual did this on the same day, that would bring the banks reserve balances with their central bank to zero, and they would be insolvent, forced to stop all bank depositors from accessing their funds, and the bank would implode overnight.

We’ve seen this movie. Yet, besides that point. Let’s focus on the money, on the actual mechanics of a wire transfer in the banking system. Besides their lack of liquidity by lending out depositor money non-consensually, putting that minor detail aside, what is actually going on inside the banks when you request a wire transfer of $100 from your bank to your friend, at his bank. How does it work under the hood?

It’s actually absurdly simple. So simple that it is nothing more than a text message sent through a text messaging network. It’s really that simple. That’s it. Nothing more. All of the fancy language about wires, and reserves and bank balances, and systemically important financial institutions and quantitative easing, blah blah blah.

It’s all just text messages on a closed privileged and licensed text messaging network.

There is a Blog by Alessa, no idea who it is, but she provides a great explanation of bank transfers from her article Fedwire: An Overview For Depository Institutions;

Fedwire® is an electronic funds transfer system operated by the twelve U.S. Federal Reserve Banks. It is used by U.S. banks, credit unions, and government agencies, as well as the Federal Reserve Banks themselves, for same-day funds transfers, otherwise known as wire transfers. U.S. branches of foreign banks or government groups may also use Fedwire, provided they maintain an account with a Federal Reserve Bank.

Fedwire is the most widely used wire transfer system in the United States, and the volume of payments it processes monthly is staggering. For example, in the month May 2021, almost 16 million wire transfers totaling $75.6 trillion were processed.

The term “wire transfer” came about in the late 1800s in the United States, when the earliest form of wire transfers was made using telegraph networks such as Western Union. Someone who wished to send money to another would give cash to one telegraph office. The telegraph operator would transmit a message to the recipient’s nearest telegraph office, which would pay the recipient in cash. The operators used passwords and code books to authorize the release of the funds to the recipient.

In essence, the money was sent “by wire.”

While the logistics have changed over the decades, the underlying principle remains the same: a wire transfer is still a message from one financial institution to another, to debit the sending party’s account and credit the receiver’s account.

In other words, the banking message is not the actual transaction. Instead the internal recording of the message is what consummates the transfer of money from one account to another, when the private ledger of each bank is updated.

And as noted in Parts One and Two of this series, those private ledgers are then presented as financial statements for outside “independent” corruptible and fallible human auditors to verify that they are following the rules of the banking messaging (accounting) system.

This is far more inefficient than Bitcoin.

With Bitcoin because there is simply one public ledger, the bitcoin message is the consummation of the transfer of money from one account to another, as the message itself is recorded to the public ledger and verified automatically by incorruptible infallible computers.

SURELY BITCOIN IS MORE THAN JUST TEXT MESSAGES!?

Well, no not really.

But, in addition to the public recording of the message, what the bitcoin text messages contain is also very unique. As explained earlier, within the banking system, the central banks can simply increase bank reserves at will, ad infinitum, by simply increasing their liabilities of depositor reserves as they purchase more and more bank assets, like government debt, corporate debt, and individual debt.

Unlike the banking system which simply provides an indication of untethered units to be transferred, in a Bitcoin message, the units to be transferred indicated by the message is referencing units that had previously been created through real world costs.

In other words, to send bitcoin from one account to another account, the bitcoin must have already been created and recorded to the public ledger. This is in sharp contrast to the modern banking system, where if a central bank wants to transfer money to a bank, it can in that moment create new bank reserves with a key stroke of the computer at essentially zero upfront cost.

In the Bitcoin system, to create bitcoin, the equivalent of Central Bank reserves, one must expend a large amount of computing energy. And the amount required is growing each day as can be seen by the hash rate of computing power growing evermore in the network. This front end cost of token creation for bitcoin allows users to have a clear picture of the expense of the system.

The actual cost of bank reserve creation in the modern banking system is seen in rising home food and energy costs, the growing increase in money supply in the banking system is paid for as price inflation that all users of the system are forced to pay. This back end expense of banking is a rather crude unquantifiable and frankly unfair mode of paying for the modern banking system.

PUBLIC INFRASTRUCTURE FOR THE WORLD

Bitcoin revolutionizes banking by starting with a fixed supply base layer, that is accessible to everyone. Today, anyone in the world can take ownership in a fixed supply monetary token we call bitcoin, and they can hold it as long as they want, seeing it accrue purchasing power over time because of its fixed supply, acting as a counterforce to the incessant monetary expansion in the modern banking system.

Because of the design of the modern banking system, the everyday users are not allowed to take custody of their money, because the money does not actually exist, it’s just a reserve balance with the central bank. With bitcoin, because its users can self custody their private key that controls the balance of their bitcoin, anyone can custody their own bitcoin which means anyone can send their bitcoin at their leisure. Anyone can send any amount of bitcoin through Bitcoins text messaging system to anyone in the world, anywhere in the world, anytime of the day, 24/7/365.

Here’s a recent talk with Jack Mallers explaining the beauty of this public infrastructure:

Everyone gets bitcoin at the price they deserve. Is today the day, you are deservant of getting Bitcoin?

In future Parts of this series we’ll dive into more details of this fascinating innovation we call Bitcoin, and the public infrastructure for the world that it truly is. We’ll look into automated lending as a replacement to the nonconsensual current lending practices of banking, automated inheritance plans thanks to the self custodial nature of Bitcoins design, as well as the forced downsizing of national governments and the ability of Bitcoin to make housing much more affordable, and so much more!

Until next time, cheers!

good article, well explained